Originally posted on

Fiercewireless just before the Christmas holiday.

2014 is nearly at and end and it's the time of the year when there are countless year-end review articles and 2015 predictions. While there were many highlights of 2014, I choose to hone in on network and competition. Instead of predictions, my 2015 expectations have been laid out with technology paths and the previous year's events.

Network

Every carrier knows that beyond service plan value and pricing, the network is the core of customer choice. It's no surprise that despite goals the carriers reach, improving, expanding and transforming the network will never really be done. Although AT&T Mobility and Verizon Wireless have reached their coverage targets, capital is still being expended to bolster networks for capacity and coverage. T-Mobile US and Sprint continue their breakneck pace to reach LTE

network parity with larger competitors.

AT&T met its

300 million POP coverage target in early September, surpassing its original end of the year target as it needed to close the gap against its main rival, Verizon. AT&T also needed to keep pace in its Voice over LTE introduction, albeit available in only in select markets. Aside from adding coverage, capacity, and expanding VoLTE in 2015, the company continues

its ambitious transformation into a software-centric network by 2020. Two big acquisitions, slated to be complete by the first half of 2015 will trigger network related work. First, the DirecTV acquisition, the company will need to fulfill its promise to provide fixed wireless broadband to rural markets. With the

acquisition of Mexican carrier Iusacell expected to close in the first quarter of next year, much of the remaining year should be laying a foundation for what AT&T touts to be the first North American mobile service area.

Sprint's 2014 travails from the "rip and replace" Network Vision program and turbulent corporate changes contributed to massive uncertainty and subscriber losses. Although the company ended the year with 260 million LTE POPs covered on its PCS spectrum,

roaming deals with rural carriers is set to expand its own LTE geographic reach to 298 million POPs in 2015. Ironically, as competitors over delivered on coverage and timing, Sprint met its end of year 100 million 2.5GHz LTE POP target, despite skepticism. In August, the 2.5 GHz buildout strategy shifted to address the heavy data consumption markets, with the logic that the popular unlimited proposition is empty without a high capacity foundation. Still, Sprint hasn't disclosed any POP targets for 2015, as it has previously.

T-Mobile over delivered and beat its own 2014 250 million POP target with 260 million covered LTE POPs. For 2014, the network story was one of aggressive execution by acquiring and deploying 700 MHz A-Block spectrum and refarming/implementing MetroPCS' spectrum to exceed its target. The company is very public about reaching an end of 2015 300 million POP target (without roaming) to close the network perception gap against larger competitors. In doing so, it will continue work to put in service remaining 700, AWS and PCS spectrum. At the same time, to get better low-band breadth, it will opportunistically purchase additional 700 MHz spectrum. However, since some regional and rural carriers will implement the same A-Block flavor, LTE roaming agreements are logical.

Though Verizon Wireless technically met the 30 million POPs covered threshold in mid-2013, the company continued to deploy and put into service AWS spectrum for capacity and fill-in. Since reaching the 300 million mark, it added 8 million more by the end of 2014. Though it has already

started refarming its PCS spectrum for LTE on a limited scale, this effort will likely continue as planned in 2015.

Technologies of Common Interest

- Carrier Aggregation: This LTE Advanced feature provides the capability to extend coverage, capacity and speed. AT&T has already started using the carrier aggregation feature mainly with its 700 and AWS assets. While AT&T does not have a national AWS footprint, it's logical that PCS spectrum that it is refarming would also be put into play. As part of its 2014 2.5 GHz buildout, Sprint stated that it was rolling out two-carrier aggregation but eventually add another carrier (end of 2015) for three-carrier aggregation to raise the speed game. T-Mobile has not said when it will deploy carrier aggregation, but it will be planned for the coming years to piece together its 700 and AWS and PCS assets. Verizon Wireless will enable carrier aggregation to its national 700 (Band 13) and AWS footprint. Given early PCS refarming and LTE deployment, there could be the technical possibility of 700 and PCS aggregation where appropriate.

One likely byproduct of all this work will be increased speed, possibly allowing one carrier to best another nationally or in specific markets. Regardless, RootMetrics is the biggest beneficiary, as every carrier have used reliability and speed claims for public relations from their reports. Behind the scenes, it's certain that carrier in-house test organizations, third party specialists Nielsen Mobile and GWS will be busy verifying.

- VoLTE: AT&T, T-Mobile and Verizon Wireless all have implemented VoLTE. Only AT&T has not claimed nationwide capability but that hasn't stopped inter-carrier interoperability activity planned for 2015. Though T-Mobile was snubbed from the press release, it would be logical that they plug in eventually. Sprint's CDMA-based HD Voice implementation and introduction leaves them out of the VoLTE club temporarily but it has a more important focus: expanding 800 MHz and 2.5 GHz LTE.

Competition

2014 was remarkable in the level of competition. Since space is short, we'll just focus on postpaid and prepaid. On the postpaid side, there were nearly 80 pricing actions and promotions from the top four carriers, not counting the numerous extensions of promotional offers. This was more than double that of 2013. Several standout service plan tools drove customer action; these included Early Termination Fee (ETF) credit, tablet data for life, double data promotions, and no money down equipment installation plans.

Carriers departed from the past practice of constantly restructuring their rate plans, gaming the right price point with the right data level. Though AT&T and Verizon changed their plans in the beginning of the year (i.e., Mobile Share to Mobile Share Value and Share Everything to More Everything) and Sprint rebooted in August

with its Family Share Pack and

iPhone for Life, limited time promotions in the back half of 2014 drove postpaid volatility and grabbed all the media headlines. Promotions gave carriers a temporary lever to address competition without permanent price drops or higher data levels.

Entering the fourth quarter, this visual graph showed the postpaid net add trending in the previous three quarters, showing T-Mobile and Verizon Wireless with good postpaid net add energy.

Source: Carrier Reports

Without full 2014 data, can we expect the same intensity of postpaid competition in 2015? It's obvious that competition will never cease in the wireless sector but there are some road signs that it won't lull.

- Sprint's need to grow: Sprint lost nearly 600,000 customers by Q3. They cannot stop the march to win back customers. Going after AT&T's and Verizon's large postpaid bases will likely continue, but how aggressive will the campaign be – sustained intensity in each quarter or pick and choose?

- T-Mobile and Sprint will continue to employ a $350 ETF switching credit. For T-Mobile, it's an "uncarrier 4.0" tenet while Sprint will need it as a necessary tool to prevent T-Mobile getting all the switching spoils.

- AT&T and Verizon won't sit back and play defense. 2014 showed that the big two hit back with their own switching and double data promotions. However, they won't be instigators.

Yet the intensity may be tempered as there were signs of financial community/investor skittishness that dropped stock prices. Industry competition is great for consumers but the wireless sector's volatility impacts

decreasing margins and perceived overpaying for future spectrum. 2014 will likely be a blowout year for T-Mobile but replicating that performance has already been downplayed at

various recent investor conferences. Rather, the thrust was about stabilizing ARPU, retention and upselling. Still, T-Mobile won't stop given their momentum.

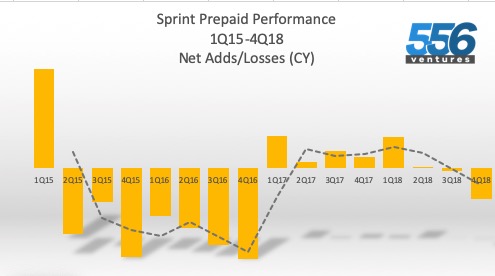

Prepaid never sees the headlines that postpaid commands. Though growth wasn't what it was in previous years, it's still hotly

contested and relevant. In prepaid, there were about 70 price and promotion actions, not counting any extensions. This was up a hair from 2013. The prepaid graph illustrates TracFone (folded in acquisitions) and T-Mobile being the big winners up to Q3.

Source: Carrier Reports

Unlike the postpaid activity predominantly occurring in the first three months and the last four months of the year, prepaid promotions and actions were evenly spread across the year. The battles for high-value monthly users consistently apply among the various TracFone brands, AT&T's Cricket, T-Mobile's MetroPCS and Sprint's Boost and Virgin Mobile brands. While price sensitivity has always been a prepaid hallmark, a shift in network and LTE marketing is broadening. Meanwhile, legacy CDMA user migration is still on the plate for Cricket and MetroPCS as each seek to move those customers onto the parent's LTE networks.

2015 competition should be spirited, as Cricket and MetroPCS will continue their head-to-head fight. Boost and Virgin will try to stay relevant in the fight while. Given postpaid's momentum, prepaid growth may be stymied at similar 2014 rates. Get the popcorn ready for next year.