Dan Meyer of RCR Wireless and I discussed the implications of the new AT&T Mobile Share Value plan and what the carriers and handset vendors are doing to get the edge in holiday sales.

Dan's article here.

Friday, December 6, 2013

Thursday, December 5, 2013

Bullet Point Analysis: New AT&T Mobile Share Value Pricing - Not Only About T-Mobile

WHAT IS IT?

There were two elements in the announcement:

ANALYSIS

TAKEAWAY: IT'S NOT ONLY ABOUT T-MOBILE BUT ALSO HITS VERIZON WIRELESS

The easiest conclusion when viewing this announcement is that AT&T is responding to T-Mobile's success of the Simple Choice no-contract plans. As T-Mobile has been very public about targeting AT&T customers, it makes sense. Yet when pricing is extracted, the results reveal interesting moves.

Back to the analysis - though the announcement lacks service pricing details, BGR.com seems to have an advance look and crafted a value chart (below) running one and two smartphone scenarios.

Graphic/table via BGR.com article.

Graphic/table via BGR.com article.

Not surprisingly, the gist of BGR's findings is that there are indeed savings. The most surprising discovery of the BGR chart (assuming the prices are correct) is that Contract customers also receive some savings relief, noted in the third column as New Price (Subsidized). This is made possible by leaks in other media that the contract smartphone device add-on is now a flat $40/month. With this as a guide, the new Value service pricing can be broken out. While there seems to be an increase at the 1 and 2 GB levels, there is some logic (explained in the Verizon Wireless impact below).

Existing AT&T business/enterprise & heavy users electing for >10GB will see the most service price savings if they make the switch.

WHAT'S IN IT FOR AT&T?

WHICH COMPANIES WILL FEEL THE MOST IMPACT?

With the above chart it is abundantly clear that AT&T was fixing non-competitive pricing against Verizon Wireless at the 6 GB to 50 GB range. Now it is at price parity in the bread and butter 2 year contract battle. Additionally, with a No-Contract option, Verizon Wireless is vulnerable for those high-value customers who want to shift over to a lesser no-contract option but won't consider T-Mobile.

COMPETITIVE RESPONSE?

There were two elements in the announcement:

- AT&T announced a no-contract option (known as Mobile Share Value) for both consumers and business customers that provides customers with plan and device discounts. New plans go in effect on Sunday, December 8. The announcement does not provide any service plan details though the carrier has stated that every smartphone added will be a flat $25/month instead of the sliding scale depending on data tier (ranging from $30-$50) on a contract offer. Also, featurephones/quick messaging devices (QMD) are now $20/month instead of $30/month. All other add-on pricing for tablets, internet devices, wireless home phones, and gaming devices remain the same.

- AT&T is adding a new Next plan 18 month upgrade option coupled with the ability to spread payments over 26 months.

ANALYSIS

TAKEAWAY: IT'S NOT ONLY ABOUT T-MOBILE BUT ALSO HITS VERIZON WIRELESS

The easiest conclusion when viewing this announcement is that AT&T is responding to T-Mobile's success of the Simple Choice no-contract plans. As T-Mobile has been very public about targeting AT&T customers, it makes sense. Yet when pricing is extracted, the results reveal interesting moves.

Back to the analysis - though the announcement lacks service pricing details, BGR.com seems to have an advance look and crafted a value chart (below) running one and two smartphone scenarios.

Not surprisingly, the gist of BGR's findings is that there are indeed savings. The most surprising discovery of the BGR chart (assuming the prices are correct) is that Contract customers also receive some savings relief, noted in the third column as New Price (Subsidized). This is made possible by leaks in other media that the contract smartphone device add-on is now a flat $40/month. With this as a guide, the new Value service pricing can be broken out. While there seems to be an increase at the 1 and 2 GB levels, there is some logic (explained in the Verizon Wireless impact below).

WHAT'S IN IT FOR AT&T?

- Though AT&T scoffs at following T-Mobile's no-contract reduced service pricing lead, the disruptive competitor has shown that the marketplace likes it. The fact that T-Mobile's last two quarters had formidable postpaid net additions helped push the AT&T decision to offer a Value plan. AT&T had to counter with something while preserving its premium brand.

- The new Mobile Share Value plans give AT&T more pricing levers. The holidays are coming up and industry insiders know that the bulk of the service providers' transactions are in Q4 and Q1. AT&T cannot allow T-Mobile (and nemesis Verizon Wireless) go into the holiday selling season with any sort of momentum.

- The new Value pricing helps the fight at the important high tier plans. This is particularly important given the target segments are heavy consumer data users and enterprise accounts, which Sprint and Verizon Wireless also covet. Moreover, these are high-value (ARPU bearing) customers that AT&T cannot afford to voluntarily churn out.

- Smartphones are where the customer and revenue growth is in the near term. By discarding the smartphone device sliding scale pricing simplifies a sales reps' ability to close a transaction. By offering a flat $40/month contract and $25/month no-contract add-on pricing, things are 'not complicated.'

- AT&T allows its contract customers to move to the new Value plans right away with fees or penalty. Contract customers will just have to remain with the carrier for the number of billing cycles they have remaining. However, they also benefit from the reduced pricing right away. While risky, this ability offsets churn, especially for those customers who don't want/need to upgrade to the latest devices at contract end.

WHICH COMPANIES WILL FEEL THE MOST IMPACT?

- T-Mobile may not get as many AT&T switchers as in previous quarters given AT&T's new No-Contract plan option. Though dismissed as expensive, AT&T's new 26 month payment extension helps to drop the per monthly device financing cost. In business accounts, T-Mobile can no longer tout that it is the only carrier with no-contract reduced service pricing.

- Verizon Wireless - In the 2 year contract world, Verizon Wireless now sees greater competition. At the low end AT&T still appears to be ahead at the 1 and 2 GB levels despite the price increase. How AT&T wins at these tiers is the new $40/mo smartphone pricing that matches Verizon Wireless'. In the old contract plan, smartphone add-ons were $45/month. In a single smartphone scenario, the 1 and 2 GB options would be $85 and $95. In the new contract plan, the same result occurs and still bests Verizon Wireless' $90 and $100. Why do it then? In order to get to a flat $40 smartphone add-on price, pricing planners needed to increase service pricing specifically at these tiers. AT&T's new 8 GB tier now allows provides price parity at the 4 GB to 10 GB range.

With the above chart it is abundantly clear that AT&T was fixing non-competitive pricing against Verizon Wireless at the 6 GB to 50 GB range. Now it is at price parity in the bread and butter 2 year contract battle. Additionally, with a No-Contract option, Verizon Wireless is vulnerable for those high-value customers who want to shift over to a lesser no-contract option but won't consider T-Mobile.

- Sprint is likely to be impacted in business accounts where it is competing heavily against AT&T and Verizon Wireless. It can't be too soon to have its Spark program rolled out to present a service differentiation.

COMPETITIVE RESPONSE?

- T-Mobile doesn't have any more pricing levers as its Simple Choice plans are fairly aggressive. Its ARPU metrics have been on the decline already and it has said that ARPU will stabilize along with churn. Along with this stability is the margin that also comes without playing the device subsidy game. Marketing and PR positioning will likely be the most logical step, marrying the value playbook with undercurrents of bolstered speed and its growing national LTE network footprint. Of course there will be the campaigns that says AT&T is copying T-Mobile.

- T-Mobile and Sprint's family plans are not shared data plans which has its own competitive merits. T-Mobile and Sprint positions the ability to assign a lesser or more data amount per user. Moreover, Sprint's unlimited proposition and lower price points still stand out compared to larger competitors Verizon Wireless and AT&T.

- Given AT&T's move into the No-Contract game, Verizon Wireless is forced to go on the same path. AT&T's no-contract $25/month smartphone add-on is fairly aggressive; Verizon Wireless would unlikely undercut this as it doesn't want to stimulate a price war. A logical and conservative scenario is to roll out a matching no-contract plan. In all likelihood, Verizon Wireless may add its own twist.

Wednesday, November 6, 2013

Sub-1GHz Spectrum in the U.S.

Today, RCR Wireless posted an Analyst Angle article that I authored on the desirability of sub-1GHz spectrum. Within the article there are some well illustrated graphics on where the top three Tier-1 providers stand in terms of coverage and spectrum depth. Here is an example for Verizon Wireless.

The control of this sub-1GHz has been long argued as a legacy competitive advantage that AT&T and Verizon Wireless has over competitors Sprint and T-Mobile. The latter carriers have decent hi-band spectrum but in order to have broad national geographic coverage, the poor propagation characteristics of 2.5 GHz (EBS and BRS) and AWS (1.7/2.1GHz) make it capital intensive and costly to mirror the sub-1GHz footprint of larger rivals.

(Thanks to Mosaik Solutions for their graphics & database work)

The control of this sub-1GHz has been long argued as a legacy competitive advantage that AT&T and Verizon Wireless has over competitors Sprint and T-Mobile. The latter carriers have decent hi-band spectrum but in order to have broad national geographic coverage, the poor propagation characteristics of 2.5 GHz (EBS and BRS) and AWS (1.7/2.1GHz) make it capital intensive and costly to mirror the sub-1GHz footprint of larger rivals.

3Q13 U.S. Tier 1 Carrier Results - A Conversation

I had a chance to talk to RCR Wireless' Dan Meyer on Tier 1 third quarter carrier results.

Read it at RCR Wireless here:: AT&T & Verizon Wireless

View it:

Read it at RCR Wireless here: Sprint and T-Mobile

View it:

Read it at RCR Wireless here:: AT&T & Verizon Wireless

View it:

Read it at RCR Wireless here: Sprint and T-Mobile

View it:

Thursday, October 10, 2013

Bullet Point Analysis: T-Mobile's Un-carrier 3.0 - The International Card

WHAT IS IT?

T-Mobile announced its Un-carrier 3.0 initiative. The 3.0 portion follows the Un-carrier strategy that the company unveiled in March 2013 to address "customers' pain points" and ultimately set the company on track to retain and grow marketshare.

As a recap, this slide from the 2013 Q2 earnings release summarizes the company's Un-carrier moves thus far.

Un-carrier 3.0 in a nutshell:

- Starting on Halloween, Simple Choice (new Uncarrier 1.0 plan) will include unlimited data and texting when roaming in 100 "Simple Global" countries.

- Voice calls are not unlimited, rather it's $0.20/minute when roaming in the 100 Simple Global countries/

- Highlights the $10 International Talk & Text add-on which allows unlimited calls to landlines in 70 countries and unlimited texts to 200 countries. Otherwise, calls are at $0.20 (or less)/minute to other countries' landlines and mobile numbers.

- Strategic Promise, Disruption and Differentiation: T-Mobile is delivering on a strategy that addresses customers' pain points. Previous iterations were doing away with contracts, early handset upgrades and lower service pricing by decoupling the overt handset subsidy. From a marketing viewpoint, this provides more advertising fodder to drive customer acquisition attack ads.

- Growing the Business Subscriber Base: Let's face it, T-Mobile has always been a consumer centric brand. Prior to its network buildout thrust, its network could not compete against larger competitors AT&T, Verizon Wireless, and Sprint, who had the business sector sewn up, especially globe trotting enterprises. In the 2Q 2013 earnings call, CEO John Legere subtlely telegraphed B2B as an area of 'coming attractions.' Legere even admitted that the "percentage of gross additions were too small to get concerned with..." With this as a backdrop, the international roaming angle of Un-carrier 3.0 is a boon to target globe trotting business customers to grow its B2B business.

- Driving International Calling: While stateside international calling can be costly for T-Mobile, one should be reminded that its prepaid brand, MetroPCS announced unlimited stateside "international" calling for $5 back in 2009. So a cost-effective (some believe VoIP-based) infrastructure is already in place.

- Impacting Profitability?: One would think before any of these moves gets off the ground, there are business cases supporting the effort. While unlimited data roaming may sound like a money loser, it's all relative for several reasons. First, the roaming impact may be thought as the cost to acquire a coveted business subscriber base that is less price sensitive than the consumer segment. The business base and the additional lines (and the overall customer spend) may offset the cost of data roaming. Second, there are parallels to the introduction of unlimited calling where a steady state and predictable monthly consumption develops. It's unlikely to think business travelers are constantly streaming video abroad - more consumer behavior. For consumers, a slower abroad data experience may provide frustration and curtail that behavior. Finally, the $10/month stateside international calling tacks helps offset some of the overall costs. Besides, as the slide above states, T-Mobile is targeting to have the lowest cost structure in the industry.

WHICH COMPANIES WILL FEEL THE MOST IMPACT?

- Clearly T-Mobile is going after its bigger competition, AT&T, Verizon Wireless and Sprint to grab business switchers. This segment tend to have higher ARPU/ARPA than consumers. The proposition is formidable as anyone who has traveled and paid for roaming can attest. Magnify this to multinational enterprises in which roaming is a substantial expense and expense managers will quickly look at T-Mobile's Uncarrier 3.0 option. T-Mobile business sales teams now have this and a growing domestic LTE national network to provide credibility in sales calls.

- It's likely that competitors will see some business subscriber leakage with a compelling offer as unlimited international data and text roaming. Competitors are already playing up slower roaming data experiences but unless they can prove that a T-Mobile roaming customer receives a slower experience than their own roaming partners, they're in the same boat (held hostage as the destination's partner network). Yet the percentage of global travel will determine an organization's business case for switching. Further, it will depend on the generation of handset for higher speed support abroad. LTE roaming is almost non-existent so the default will be HSPA+ (in some countries dual carrier HSPA+ is possible) or EDGE roaming.

- A possible scenario may be that T-Mobile 'lines' will be purchased for international business. This approach will provide a known US number for easy contact rather than to purchase an in-country SIM card. So the customer may have both a domestic and international phone/line. Either way, T-Mobile stands to gain subscriber lines and if they can prove domestic network parity in the long term, total switching will become a viable scenario.

- On the stateside international calling front, VoIP providers such as Skype may feel some impact as the simple ability to direct dial can trump launch an OTT app on a computer or handset.

COMPETITIVE RESPONSE?

It remains to be seen if competitors will match T-Mobile's unlimited data and text roaming offer. To some extent, they are handcuffed as their enterprise bases are large and international roaming revenue, decently profitable. Loyalty and network breadth (domestic and international) will be a piece of the counter argument. However, Un-carrier 3.0 is a formidable challenge that will need to be addressed. Key indicators will be customer inquiry for a competitive response, roaming revenue declines and customer voluntary churn. What form it will take and how quickly a solution rolls out depends on customer defection. Regardless, product planners will be in meetings to figure out their company's response alternatives.

Thursday, August 22, 2013

Tier One Carriers' Chief Marketing Officers

The U.S. wireless landscape continues to evolve with elevated competition. The stakes are higher now as postpaid subscriber growth of years past now declines. Postpaid switching (stealing subscribers) is the new battleground while, in parrallel, acquiring high-value prepaid customers has stepped up in urgency. Add to this, increasing the wholesale customer base, which includes MVNOs and machine-to-machine (including the nascent automobile infotainment), is an added necessity.

While the Chief Executive Officers and Chief Financial Officers get the limelight of quarterly earnings calls and investor conferences, the Chief Marketing Officer (CMO) has the responsibility to further/preserve the corporation's brand equity, and create strategies to help grow the customer base. With the ultra-competitive nature of the American wireless sector, let's see who is steering the Tier One carriers' marketing and directing campaigns against rivals. The following biographies are taken off the respective corporate websites:

AT&T Mobility - David Christopher

David Christopher, chief marketing officer, AT&T Mobility, leads product strategy, marketing and execution across AT&T’s extensive portfolio of branded wireless communications services and devices.

David Christopher, chief marketing officer, AT&T Mobility, leads product strategy, marketing and execution across AT&T’s extensive portfolio of branded wireless communications services and devices.

His responsibilities include overall product direction and planning for branded wireless services, including voice, data and cloud products, devices and accessories and network marketing; national, channel and field marketing – including the marketing strategy and merchandizing for AT&T’s more than 2,400 company owned retail stores; youth and diversity marketing; market research; customer lifecycle management; promotions and pricing; and national advertising and strategic sponsorships.

Christopher also oversees the award-winning AT&T Developer Program and its more than 25,000 members, leading the team that determines and delivers the tools and training developers need to build new and innovative applications.

Previously, Christopher served as chief marketing officer for AT&T’s Mobility and Consumer Markets, which included leading all marketing and product functions that drove the company’s three-screen strategy across wireless, TV and broadband products. He also served as vice president of product management for AT&T’s wireless unit, Cingular Wireless.

Before joining AT&T, Christopher worked at Palm, serving most recently as vice president – Product Marketing and Management with responsibility for the team that defined, developed and managed all Palm-branded product lines worldwide from concept through end of life.

Prior to Palm, Christopher worked for Sara Lee Corporation in Barcelona, Spain and Gent, Belgium.A native of Winston-Salem, NC, Christopher earned a bachelor’s degree from the University of Virginia and a Masters of Business Administration from the Kellogg School at Northwestern University.

Christopher serves on the Ad Council’s board of directors and its executive committee and on the Facebook Client Council.

Sprint - Bill Malloy

Bill Malloy joined Sprint in September 2011 as chief marketing officer.

Bill Malloy joined Sprint in September 2011 as chief marketing officer.

G. Michael (Mike) Sievert, age 44, serves as our Executive Vice President and Chief Marketing Officer. Mr. Sievert is responsible for strategic development and execution of all marketing, product development, and pricing programs and activities for the Company. Mr. Sievert has also served as Executive Vice President and Chief Marketing Officer of T-Mobile USA since November 2012. Prior to joining T-Mobile USA, Mr. Sievert was an entrepreneur and investor involved with several Seattle-area start-up companies, most recently serving as CEO of Discovery Bay Games, a maker of accessories and add-ons for tablet computers, from April 2012 to November 2012. From April 2009 to June 2011, he was Chief Commercial Officer at Clearwire Corporation, a broadband communications provider, responsible for all customer-facing operations. From February 2008 to January 2009, Mr. Sievert was co-founder and CEO of Switchbox Labs, Inc., a consumer technologies developer, leading up to its sale to Lenovo. He also served from January 2005 to February 2008 as Corporate Vice President of the worldwide Windows group at Microsoft Corporation, responsible for global product management and P&L performance for that unit. Prior to Microsoft, he served as Executive Vice President and Chief Marketing Officer at AT&T Wireless for three years. He also served as Chief Sales and Marketing officer at E*TRADE Financial and began his career with management positions at Procter & Gamble and IBM. He has served on the boards of Rogers Wireless in Canada, Switch & Data Corporation, and a number of technology start-ups. Mr. Sievert received a Bachelor’s degree in Economics from the Wharton School at the University of Pennsylvania.

G. Michael (Mike) Sievert, age 44, serves as our Executive Vice President and Chief Marketing Officer. Mr. Sievert is responsible for strategic development and execution of all marketing, product development, and pricing programs and activities for the Company. Mr. Sievert has also served as Executive Vice President and Chief Marketing Officer of T-Mobile USA since November 2012. Prior to joining T-Mobile USA, Mr. Sievert was an entrepreneur and investor involved with several Seattle-area start-up companies, most recently serving as CEO of Discovery Bay Games, a maker of accessories and add-ons for tablet computers, from April 2012 to November 2012. From April 2009 to June 2011, he was Chief Commercial Officer at Clearwire Corporation, a broadband communications provider, responsible for all customer-facing operations. From February 2008 to January 2009, Mr. Sievert was co-founder and CEO of Switchbox Labs, Inc., a consumer technologies developer, leading up to its sale to Lenovo. He also served from January 2005 to February 2008 as Corporate Vice President of the worldwide Windows group at Microsoft Corporation, responsible for global product management and P&L performance for that unit. Prior to Microsoft, he served as Executive Vice President and Chief Marketing Officer at AT&T Wireless for three years. He also served as Chief Sales and Marketing officer at E*TRADE Financial and began his career with management positions at Procter & Gamble and IBM. He has served on the boards of Rogers Wireless in Canada, Switch & Data Corporation, and a number of technology start-ups. Mr. Sievert received a Bachelor’s degree in Economics from the Wharton School at the University of Pennsylvania.

Verizon Wireless - Ken Dixon

Ken Dixon is vice president and chief marketing officer for Verizon Wireless, the largest wireless company in the United States, with responsibility for all brand management and marketing initiatives for the company, including the management and development of mobile products and services, media buying, agency management and website integration. A premier technology company, Verizon Wireless operates the nation’s largest and most reliable 4G LTE network.

Ken Dixon is vice president and chief marketing officer for Verizon Wireless, the largest wireless company in the United States, with responsibility for all brand management and marketing initiatives for the company, including the management and development of mobile products and services, media buying, agency management and website integration. A premier technology company, Verizon Wireless operates the nation’s largest and most reliable 4G LTE network.

While the Chief Executive Officers and Chief Financial Officers get the limelight of quarterly earnings calls and investor conferences, the Chief Marketing Officer (CMO) has the responsibility to further/preserve the corporation's brand equity, and create strategies to help grow the customer base. With the ultra-competitive nature of the American wireless sector, let's see who is steering the Tier One carriers' marketing and directing campaigns against rivals. The following biographies are taken off the respective corporate websites:

AT&T Mobility - David Christopher

His responsibilities include overall product direction and planning for branded wireless services, including voice, data and cloud products, devices and accessories and network marketing; national, channel and field marketing – including the marketing strategy and merchandizing for AT&T’s more than 2,400 company owned retail stores; youth and diversity marketing; market research; customer lifecycle management; promotions and pricing; and national advertising and strategic sponsorships.

Christopher also oversees the award-winning AT&T Developer Program and its more than 25,000 members, leading the team that determines and delivers the tools and training developers need to build new and innovative applications.

Previously, Christopher served as chief marketing officer for AT&T’s Mobility and Consumer Markets, which included leading all marketing and product functions that drove the company’s three-screen strategy across wireless, TV and broadband products. He also served as vice president of product management for AT&T’s wireless unit, Cingular Wireless.

Before joining AT&T, Christopher worked at Palm, serving most recently as vice president – Product Marketing and Management with responsibility for the team that defined, developed and managed all Palm-branded product lines worldwide from concept through end of life.

Prior to Palm, Christopher worked for Sara Lee Corporation in Barcelona, Spain and Gent, Belgium.A native of Winston-Salem, NC, Christopher earned a bachelor’s degree from the University of Virginia and a Masters of Business Administration from the Kellogg School at Northwestern University.

Christopher serves on the Ad Council’s board of directors and its executive committee and on the Facebook Client Council.

Sprint - Bill Malloy

Malloy brings to Sprint more than 30 years of experience in senior operating roles with marketing, media and wireless companies ranging from start-up ventures to large corporate entities.

He has been involved in the wireless industry almost since its inception in the mid-1980s, holding key marketing and operational leadership positions with McCaw Cellular and AT&T Wireless.

Most recently he was a venture partner with Ignition Partners, a venture capital firm based in Seattle. He joined Ignition in 2002 and during the next seven years was a member of the firm’s wireless communications team. In addition to working on early-stage investments, he represented the firm from 2004 to 2009 as chairman and CEO of Sparkplug Communications, a company created from within Ignition that later merged with Airband Communications. Before Ignition, he served as CEO of two Internet companies, Peapod and Worldstream Communications.

During his tenure at McCaw Cellular and AT&T Wireless he served as executive vice president of U.S. operations for AT&T Wireless, leading the team that created and launched AT&T’s Digital One Rate, the first national wireless calling plan. Before that, he was president of the company’s central region and led the build-out and launch of AT&T PCS markets. He also served as regional vice president of McCaw Cellular’s operations in Oklahoma, Arkansas, Kansas and Missouri and led national marketing for the company during the launch of Cellular One, the first national wireless brand for independent carriers, and the North American Cellular Network (NACN), the first national wireless call delivery network.

Malloy began working with McCaw in 1985 when he was a partner with the company's advertising agency. Before joining McCaw Cellular, he had an 11-year career in senior operating and partner positions in advertising firms and media companies.

Malloy is a graduate of Washburn University and Northwestern University’s Kellogg Graduate School of Management where he graduated from the Kellogg Management Institute.

Malloy is a graduate of Washburn University and Northwestern University’s Kellogg Graduate School of Management where he graduated from the Kellogg Management Institute.

T-Mobile - Michael Sievert

Verizon Wireless - Ken Dixon

{kind=link}

Previously, Dixon served as president, Midwest Area for Verizon Wireless, where he was responsible for the company’s operations in the Great Plains, Illinois/Wisconsin, Kansas/Missouri, Michigan/Indiana/Kentucky and Ohio/Pennsylvania/West Virginia regions.

Dixon has also served as region president for the company’s Georgia/Alabama, Upstate New York and New England Regions where he was responsible for overseeing general operations and sales leadership. He also served as vice president of Operations and Distribution in the Mid-Atlantic Area and managed business and indirect sales in the Upstate New York and New England Regions.

Dixon joined the wireless industry in 1992 and has since held several management positions in both sales and operations. He earned a bachelor’s degree from Syracuse University in Syracuse, NY.

Observations

Tenures:

- AT&T's Christopher has been at the helm since April 2007 when previous CMO Marc LeFar (now Vonage CEO) resigned. He has product, service and marketing stints in his past. From that perspective, he understands the mobility business as well as the fixed line consumer side.

- Sprint's Malloy became Sprint's formal CMO in April 2011. The position had been vacant ever since Dan Hesse took the helm in 2007. In the years running up to 2011, Hesse had not appointed anyone into the title. But Bill Morgan (now SVP - Marketing at Motorola Mobility) had the overall marketing responsibility until 2011. As an old AT&T Wireless, McCaw Cellular hand, he understands the services and products space. Moreover, his internet/start-up/VC and advertising background gives him well-rounded overall marketing credentials.

- Mike Sievert, seemingly, is the newest CMO in this peer group also with product, services and software background. The T-Mobile CMO job has relatively high turnover compared to other Tier Ones. He came on to the scene replacing acting-CMO Andrew Sherrard (still an SVP in Marketing and replaced Cole Brodman May 2012) in mid-November 2012, a month after CEO John Legere took the helm.

- Verizon Wireless' Ken Dixon replaced Marni Walden (now Chief Operating Officer who took the post in 2010). There aren't any news releases on when Dixon took the position. As late as February 2012, he was the President of the Midwest region so presumably, it was in 2012 or 2013. Ken Dixon's stints in multiple regional president roles give him both regional and national operational (sales and service) and marketing sensitivities, since regions have the autonomy to do complementary local marketing.

Each companies' marketing organizations have their own strengths and challenges but that will be for another post.

Thursday, July 25, 2013

Bullet Point Analysis: MetroPCS's 15 New Market Expansion & New Handsets

MetroPCS had multiple announcements. The first announcement focuses on expanded its smartphone portfolio with the Nokia Lumia 521 ($99) and LG Optimus F3 ($149). While handset announcements are less than notable on a strategy, there are small tidbits that one can glean. They are:

The second press release was more interesting. MetroPCS announced 15 new markets, expanding their total market reach to 30 markets. With this announcement, the company has opened up for business in those markets along with distribution. However, Metro will wait until September 1 for their advertising push.

Of the 15 markets, 8 are Leap markets. T-Mobile's CEO has talked up a head-to-head match up against Leap. Interestingly some are in Texas, a Leap stronghold. One symbolic market that stands out is San Diego - Leap's corporate headquarters. Key to the success will obviously be distribution - big box stores such as Best Buy and third party retailers. The company is looking for 200 doors in August with more in the fall.

- The smartphones are not CDMA. This is a step to migrate the subscriber base to the T-Mobile network (100% goal in 2015) .

- The Lumia is an HSPA+ only device and comes from the T-Mobile prepaid device stable. Moreover, it give MetroPCS a Windows Phone choice.

- The LG Optimus F3 is HSPA+/LTE. Other carriers have the F3 in CDMA configuration. The F3 has better processor specs than the postpaid Optimus L9 offering. So the prepaid version bests a postpaid offering, albeit a tad smaller (4" vs 4.5" screen).

The second press release was more interesting. MetroPCS announced 15 new markets, expanding their total market reach to 30 markets. With this announcement, the company has opened up for business in those markets along with distribution. However, Metro will wait until September 1 for their advertising push.

Of the 15 markets, 8 are Leap markets. T-Mobile's CEO has talked up a head-to-head match up against Leap. Interestingly some are in Texas, a Leap stronghold. One symbolic market that stands out is San Diego - Leap's corporate headquarters. Key to the success will obviously be distribution - big box stores such as Best Buy and third party retailers. The company is looking for 200 doors in August with more in the fall.

- Baltimore, MD - Head-to head against Leap/Cricket

- Birmingham, Ala. - New market without retail Leap presence; Next major city that links up with Atlanta market

- Cleveland and Akron, Ohio - adds to Great Lakes coverage

- Corpus Christi, Texas - Head-to head against Leap/Cricket

- Fresno, Calif. - Head-to head against Leap/Cricket

- Houston, Texas - Head-to head against Leap/Cricket

- Memphis, Tenn. - Head-to head against Leap/Cricket

- New Orleans, LA - New market without retail Leap presence

- Rio Grande Valley, Texas - Head-to head against Leap/Cricket

- San Antonio and Austin, Texas - Head-to head against Leap/Cricket

- San Diego, Calif. - In Leap's backyard (its headquarters)

- Seattle and Tacoma, Wash. - In T-Mobile's HQ area, no brainer in opening up distribution in the parent's backyard; New market without retail Leap presence

- Tallahassee, Fla. - Rounds out MetroPCS's Florida coverage. New market without retail Leap presence

- Toledo and Sandusky, Ohio - adds to Great Lakes coverage; New market without retail Leap presence

- Washington, DC - Head-to head against Leap/Cricket

Tuesday, July 16, 2013

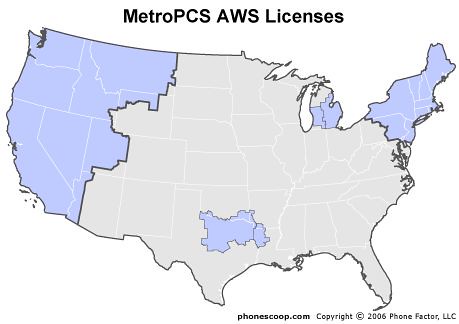

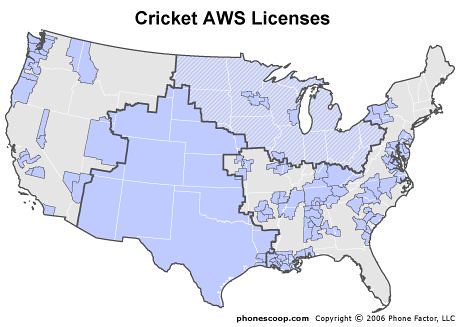

AWS Spectrum Maps - Before and After: AT&T-Leap Buyout

In yesterday's post, we saw the results of a combined entity spectrum depth map that displayed the 700MHz, Cellular, PCS and AWS bands. However, one of the points I brought up was AT&T staying in the AWS spectrum game for LTE capacity fill in (to 700) and to position itself from an AWS LTE roaming standpoint. In this post, we are fortunate to show the AWS holdings for Leap and AT&T.

Leap AWS spectrum

Combined AT&T-Leap AWS spectrum

What have we concluded? Specifically, the AWS national footprint still far from filled as evidenced by the white on the map. Once AWS LTE roaming happens, AT&T has the option to fill those areas, if necessary.

Despite the AWS gaps, we can see that Leap will strength AT&T LTE in specific markets such as:

Thanks to Mosaik for their output.

Thanks to Mosaik for their output.

Leap AWS spectrum

AT&T AWS spectrum

What have we concluded? Specifically, the AWS national footprint still far from filled as evidenced by the white on the map. Once AWS LTE roaming happens, AT&T has the option to fill those areas, if necessary.

Despite the AWS gaps, we can see that Leap will strength AT&T LTE in specific markets such as:

- (West) Seattle, central California, San Diego, Salt Lake City, Denver

- (Southwest) Las Vegas, Phoenix, Tuscon, Sante Fe, El Paso

- (Midwest) Kansas City, Omaha, Chicago, Milwaukee, St. Louis, Cincinnati, Louisville, Nashville

- (South-ish) San Antonio, Ok City, New Orleans, Little Rock, Memphis, Hashville

- (Mid-Atlantic) Baltimore, Philadelphia, Washington, DC, Richmond, Charlotte, Raleigh, Columbia

- (East-ish) Buffalo, Pittsburgh

Again, the combined AT&T-Leap spectrum depth map (note this excludes WCS spectrum)

Monday, July 15, 2013

The AT&T-Leap Spectrum Depth (A Map View)

Spectrum is indeed a prime factor in any wireless carrier acquisition. Spectrum maps play an important role in understanding deal motivation and what the resulting merged entities' national spectrum depth looks like.

The Leap spectrum view:

Though Leap's spectrum (mainly PCS and AWS (the 700 in Chicago is for sale)) goes beyond their operating regional markets, the company's business model focuses in on densely populated markets.

Though Leap's spectrum (mainly PCS and AWS (the 700 in Chicago is for sale)) goes beyond their operating regional markets, the company's business model focuses in on densely populated markets.

The AT&T spectrum view:

With the Leap spectrum, AT&T is strengthened in some heavily contested markets including, the Mid-Atlantic, central California, Las Vegas (better AT&T service at CTIA?), Denver, KC (Sprint's backyard), St. Louis (Sprint's newest market acquisition from US Cellular), and Northwest (Seattle - T-Mobile's backyard). Of course, the big question is will spectrum need to be divested? The Department of Justice uses the Herfindahl-Hirschman Index (HHI) to measure market concentration for purposes of antitrust enforcement.

Note: Thanks to Mosaik for the use of their MapElements output.

The Leap spectrum view:

The AT&T spectrum view:

The combined AT&T-Leap spectrum view:

With the Leap spectrum, AT&T is strengthened in some heavily contested markets including, the Mid-Atlantic, central California, Las Vegas (better AT&T service at CTIA?), Denver, KC (Sprint's backyard), St. Louis (Sprint's newest market acquisition from US Cellular), and Northwest (Seattle - T-Mobile's backyard). Of course, the big question is will spectrum need to be divested? The Department of Justice uses the Herfindahl-Hirschman Index (HHI) to measure market concentration for purposes of antitrust enforcement.

Note: Thanks to Mosaik for the use of their MapElements output.

Sunday, July 14, 2013

Bullet Point Analysis: The AT&T-Leap Buyout

What is it?

AT&T is buying prepaid player Leap Wireless for $15 per share in cash. Under the terms of the agreement, AT&T will acquire all of Leap’s stock and wireless properties, including licenses, network assets, retail stores and approximately 5 million subscribers. AT&T expects the transaction to complete in 6-9 months (1H 2014).

What is in it for Leap?

- For shareholders and management, they can exit the cut throat prepaid business with money. Leap and similar regional prepaid player, MetroPCS, had once enjoyed strong growth until a couple of years ago. National competitors and prepaid MVNOs ate into their marketshare and growth. T-Mobile's acquisition of MetroPCS that closed in May 2013 logically put a brighter spot light on Leap.

- For Leap operations, the Cricket brand expands its geographical reach beyond Leap's limited regional footprint and can go head-to-head against MetroPCS and can tap into AT&T's distribution resources.

- For the Leap network, it has a clearer LTE path. Operating CDMA (96M POPs) and LTE (21M POPs) in the same limited AWS spectrum bands doesn't work well.

What is in it for AT&T?

Spectrum:

- Complementary PCS and AWS bands covering 137M POPs, some of AWS is not in service (41M POPs).

- Proceeds from the Leap 700 A Block spectrum goes into the deal calculus.

Subscribers and Doors:

- Leap has 5 million prepaid subscribers but the company has been trying to right itself after steady customer losses that began in Q2 2012. AT&T increases its prepaid customer base to roughly 12 million, roughly 11% of the AT&T total subscriber base.

- Leap's distribution channel numbers a little less than 9,000 doors.

- Commentary: Leap's business needs a turnaround that Leap's management has been trying to accomplish for more than a year. In that time, Leap lost about 900K customers. Leap's distribution also slimmed down from over 11K doors in a bid to focus customer acquisition. AT&T's own branded prepaid is not growing. The launch of the Aio brand in May allows for the company to enter the prepaid market aggressively without diminishing the AT&T brand. Now that Leap joins the AT&T prepaid fight, the strategy is shaping up to match the segmentation strategy pioneered by Sprint (Boost, Virgin, Assurance) and Tracfone (Tracfone, StraightTalk, Net10, Simple Mobile, PagePlus, and Safelink). T-Mobile also joins in the prepaid segmentation fight with its own GoSmart and MetroPCS). All this Tier-1 competition and the plethora of MVNOs out there vying for the prepaid share of wallet will make for thin margins.

Keeping T-Mobile Away: There are many who say this is a spectrum deal. That is true that additional PCS and AWS spectrum enhances the AT&T network, I argue that a large element is to neutralize a growing T-Mobile threat. Fresh off the May close of MetroPCS, T-Mobile supplemented its AWS spectrum with a $308M deal with US Cellular at the end of June.

Graphics from Phonescoop.com

But with the AT&T-T-Mobile merger breakup, T-Mobile received some AWS licenses and in 2012, Leap and T-Mobile traded some licenses. While the T-Mobile-MetroPCS coverage map looks empty in some areas of the country, that is not to say that the company lacks spectrum in those areas.

As seen in the spectrum holdings graphic, the company does indeed have spectrum nationally and can expand if so desired.

With the June purchase of Mississippi Valley AWS spectrum from US Cellular (Barat) Wireless) and a future rumored purchase of Leap, the T-Mobile AWS portfolio would be formidable. Aside from T-Mobile, archrival Verizon Wireless' SpectrumCo AWS deal completed in August 2012 and building out this AWS to add LTE network capacity.

This competitive landscape would put AT&T in an AWS coverage disadvantage relative to T-Mobile and Verizon Wireless. Therefore, AT&T needed to stay in the AWS LTE game and keep T-Mobile from growing a stronger AWS portfolio. For AT&T, AWS will not only to serve to add LTE capacity customers but also tap into future AWS LTE roaming revenue. T-Mobile, AT&T and Verizon Wireless are logical future roaming partners.

Which companies will feel the most impact?

- For T-Mobile, with Leap as a unit of AT&T, its MetroPCS geographic expansion will be challenged by AT&T's resources. T-Mobile seemingly has a year or two lead as it is integrating MetroPCS and working on migrating the CDMA base to HSPA+/LTE but the stated goal of 2015.

- Sprint will lose 3G data wholesale revenue from the agreement forged in August 2010 that expires in Dec 2015. But now Sprint (Clearwire's owner) loses another wholesale arrangement that Clearwire announced in March 2012 though nothing really started. It's clear now that Sprint's prepaid segmentation strategy was the correct in the long run but Aio Wireless and Cricket are going up against Virgin, Boost, Assurance, respectively. Cricket's logical national (or specific target market) expansion may spell trouble.

- Verizon Wireless now sees a stronger AT&T rival with new found AWS and PCS spectrum from Leap. In the long term, it needs additional spectrum to thwart impending capacity brought on with WCS and Channel 55 (700 from Qualcomm) frequencies. In terms of prepaid, its branded prepaid is holding its own but without any flanker brands, competitors will take almost all the future prepaid growth.

- In infrastructure, AT&T LTE equipment suppliers, Alcatel and Ericsson now have more of an order pipeline than before.

Last Word

- The biggest question in this deal is whether the acquisition will pass regulatory hurdles. The sting of the failure to acquire T-Mobile is still fresh in everyone's minds. Like any major deal, it should have been gamed out by M&A internal and external resources taking into account the regulatory environment before it makes the light of day.

- If regulatory hurdles are overcome, what conditions will there be? AT&T has proactively said that the Chicago 700 MHz A Block will be sold. (It doesn't like the A block anyway). Will the company need to divest in other markets (planned or unplanned)?

Wednesday, July 10, 2013

Analysis: T-Mobile’s "Boldest" Move - JUMP and Simple Choice forFamilies

What is it?

- T-Mobile announced an equipment upgrade program known as JUMP!™, which enables people to upgrade their phones when they want, up to twice a year as soon as six months from enrollment. The monthly outlay is $10/month with equipment warranty (theft, lost, broken, or when one wants another phone).

- The Simple Choice for Family plan (4 lines of unlimited talk, text and web(500MB) for $100/month) was also announced allowing access to discounted plans without a credit check. The caveat is that payment must be in advance (prepaid).

- JUMP Details:

- Enroll in JUMP for $10/month. Have to wait for 6 months until the first 'JUMP' to get a new device.

- If in 'Good Working Order' (powers on, no screen cracks, no visible water damage), customer can get the next latest and greatest. If customer is financing it (Equipment Installment Plan (EIP)), remainder of payments are waived. Customer can enter a new EIP plan.

- If not in 'Good Working Order,' a deductible will be paid ranging from $20-$170, depending on device,

- Customer can upgrade twice a year. It could be as early as the next day.

What it means for

consumers:

- For T-Mobile consumers who are early adopters and want the latest and greatest, Jump should be very compelling.

- For T-Mobile customers who don't care for upgrading and are price-sensitive, they're not likely to enroll in JUMP as the enrollment tallies to $120 a year.

- For credit challenged family customers who want access to discounted postpaid rates, this should spur them on.

- The JUMP plan should appeal for early adopters in other competitors. Since T-Mobile is targeting AT&T, it would be logical for T-Mobile to step up some anti-AT&T marketing as it has done so already.

- JUMP is an interesting anti-churn tool that appeals to a segment of customer who is willing to switch to get the latest and greatest. For this reason, it comports with T-Mobile's public comments stating that 2013 is going to be a year to stabilize.

- JUMP may be an effective switching tool. If T-Mobile can convince potential switchers that the T-Mobile network is just as good as everyone else's that would help customer acquisition.

- The long term impact of JUMP 'trade-in' devices will help its MetroPCS unit. These turned in devices will be refurbished and pushed into the MetroPCS portfolio as refurbished. For the MetroPCS customer who normally pays full priced for a phone, access to nearly the latest and greatest smartphone at a lower cost increases service stickiness. As T-Mobile wants to transition MetroPCS customers from their CDMA phones anyway, this move can potentially help accelerate the migration to the LTE/HSPA network and refarming of MetroPCS PCS spectrum.

- Depending upon the JUMP subscriber size, the $10 monthly fee may be a factor in lifting postpaid ARPU.

- Simple Choice for Family should also help T-Mobile acquire subscribers. The price point is compelling. This plan could draw price sensitive postpaid family subscribers from competitors as well as transition families dealing with individual prepaid plans. How much this will hit Tracfone brands like StraightTalk and Simple Mobile remains to be seen. Of note, Simple Choice is LTE accessible whereas MVNO plans are still 3G/HSPA (okay 4G-ish).

·

Which companies will

feel the most impact?

- AT&T as the very public target should see the most marketing against its subscribers. Other competitors may experience some leakage from their early adopter community as well, especially those whose ending contracts.

- T-Mobile warranty companies should be busy depending upon how well JUMP is embraced.

- Handset makers (likely with halo devices) will likely see more volume coming out of T-Mobile. With increased volume, T-Mobile may leverage this to attain more favorable pricing.

Thursday, June 27, 2013

DISH Folds & Some DISH Options

Poker

As the long multi-hand poker game with Sprint, DISH, Softbank and Clearwire dragged on with DISH upping the ante, forcing Sprint and Softbank to push, DISH folded on both deals in the end.

DISH's game to takeover Sprint ended on June 18, 2013 when they withdrew their offer. The press release language implied that they will devote their resources to win Clearwire. It didn't look bad when the Clearwire board recommended DISH's offer back on June 12.

DISH folded on its second poker hand with yesterday's June 26 announcement. Many including me, expected another run, upping the ante, given DISH's playing profile but what did it have to gain? Really - nothing.

DISH's Options

The near term scenario is that DISH needs to get service up and running. Any time you're delayed means lost future revenue opportunity. With its core business slipping, there is urgency to get into the mobile space. Given this line of thought, it needs to bury the hatchet with Sprint and move to spectrum hosting.

A long term scenario is that DISH can wait until an alternate hosting provider comes on line. T-Mobile has been bandied about as that partner. But why not Verizon Wireless and AT&T? Everyone wants access to new spectrum and if the deal is right, anything is possible.

Regardless of scenario, DISH and a partner(s) need to seed the mobile ecosystem on DISH's bands. Technically, it may not be a stretch. However, the lead times to quickly create/productize the chipsets and integrate into production hardware (device and infrastructure) are still an issue. Once it joins the mobile service provider club, DISH can upsell its own customers on mobile broadband (either fixed or mobile) and wholesale its capacity.

Looking ahead, DISH is looking for another game but it may not be poker.

Subscribe to:

Posts (Atom)