What is it?

AT&T is buying prepaid player Leap Wireless for $15 per share in cash. Under the terms of the agreement, AT&T will acquire all of Leap’s stock and wireless properties, including licenses, network assets, retail stores and approximately 5 million subscribers. AT&T expects the transaction to complete in 6-9 months (1H 2014).

What is in it for Leap?

- For shareholders and management, they can exit the cut throat prepaid business with money. Leap and similar regional prepaid player, MetroPCS, had once enjoyed strong growth until a couple of years ago. National competitors and prepaid MVNOs ate into their marketshare and growth. T-Mobile's acquisition of MetroPCS that closed in May 2013 logically put a brighter spot light on Leap.

- For Leap operations, the Cricket brand expands its geographical reach beyond Leap's limited regional footprint and can go head-to-head against MetroPCS and can tap into AT&T's distribution resources.

- For the Leap network, it has a clearer LTE path. Operating CDMA (96M POPs) and LTE (21M POPs) in the same limited AWS spectrum bands doesn't work well.

What is in it for AT&T?

Spectrum:

- Complementary PCS and AWS bands covering 137M POPs, some of AWS is not in service (41M POPs).

- Proceeds from the Leap 700 A Block spectrum goes into the deal calculus.

Subscribers and Doors:

- Leap has 5 million prepaid subscribers but the company has been trying to right itself after steady customer losses that began in Q2 2012. AT&T increases its prepaid customer base to roughly 12 million, roughly 11% of the AT&T total subscriber base.

- Leap's distribution channel numbers a little less than 9,000 doors.

- Commentary: Leap's business needs a turnaround that Leap's management has been trying to accomplish for more than a year. In that time, Leap lost about 900K customers. Leap's distribution also slimmed down from over 11K doors in a bid to focus customer acquisition. AT&T's own branded prepaid is not growing. The launch of the Aio brand in May allows for the company to enter the prepaid market aggressively without diminishing the AT&T brand. Now that Leap joins the AT&T prepaid fight, the strategy is shaping up to match the segmentation strategy pioneered by Sprint (Boost, Virgin, Assurance) and Tracfone (Tracfone, StraightTalk, Net10, Simple Mobile, PagePlus, and Safelink). T-Mobile also joins in the prepaid segmentation fight with its own GoSmart and MetroPCS). All this Tier-1 competition and the plethora of MVNOs out there vying for the prepaid share of wallet will make for thin margins.

Keeping T-Mobile Away: There are many who say this is a spectrum deal. That is true that additional PCS and AWS spectrum enhances the AT&T network, I argue that a large element is to neutralize a growing T-Mobile threat. Fresh off the May close of MetroPCS, T-Mobile supplemented its AWS spectrum with a $308M deal with US Cellular at the end of June.

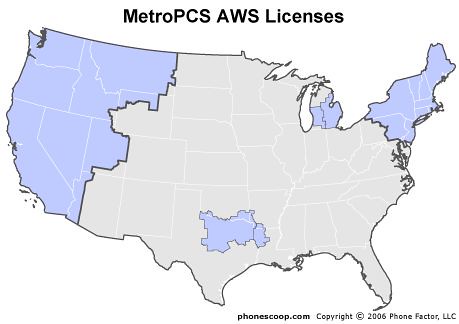

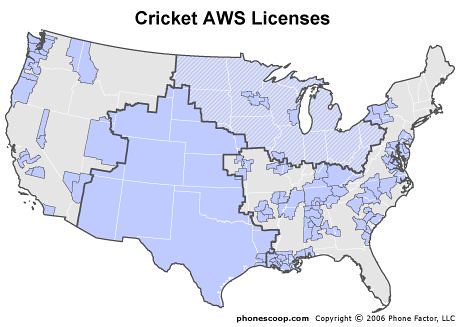

Graphics from Phonescoop.com

But with the AT&T-T-Mobile merger breakup, T-Mobile received some AWS licenses and in 2012, Leap and T-Mobile traded some licenses. While the T-Mobile-MetroPCS coverage map looks empty in some areas of the country, that is not to say that the company lacks spectrum in those areas.

As seen in the spectrum holdings graphic, the company does indeed have spectrum nationally and can expand if so desired.

With the June purchase of Mississippi Valley AWS spectrum from US Cellular (Barat) Wireless) and a future rumored purchase of Leap, the T-Mobile AWS portfolio would be formidable. Aside from T-Mobile, archrival Verizon Wireless' SpectrumCo AWS deal completed in August 2012 and building out this AWS to add LTE network capacity.

This competitive landscape would put AT&T in an AWS coverage disadvantage relative to T-Mobile and Verizon Wireless. Therefore, AT&T needed to stay in the AWS LTE game and keep T-Mobile from growing a stronger AWS portfolio. For AT&T, AWS will not only to serve to add LTE capacity customers but also tap into future AWS LTE roaming revenue. T-Mobile, AT&T and Verizon Wireless are logical future roaming partners.

Which companies will feel the most impact?

- For T-Mobile, with Leap as a unit of AT&T, its MetroPCS geographic expansion will be challenged by AT&T's resources. T-Mobile seemingly has a year or two lead as it is integrating MetroPCS and working on migrating the CDMA base to HSPA+/LTE but the stated goal of 2015.

- Sprint will lose 3G data wholesale revenue from the agreement forged in August 2010 that expires in Dec 2015. But now Sprint (Clearwire's owner) loses another wholesale arrangement that Clearwire announced in March 2012 though nothing really started. It's clear now that Sprint's prepaid segmentation strategy was the correct in the long run but Aio Wireless and Cricket are going up against Virgin, Boost, Assurance, respectively. Cricket's logical national (or specific target market) expansion may spell trouble.

- Verizon Wireless now sees a stronger AT&T rival with new found AWS and PCS spectrum from Leap. In the long term, it needs additional spectrum to thwart impending capacity brought on with WCS and Channel 55 (700 from Qualcomm) frequencies. In terms of prepaid, its branded prepaid is holding its own but without any flanker brands, competitors will take almost all the future prepaid growth.

- In infrastructure, AT&T LTE equipment suppliers, Alcatel and Ericsson now have more of an order pipeline than before.

Last Word

- The biggest question in this deal is whether the acquisition will pass regulatory hurdles. The sting of the failure to acquire T-Mobile is still fresh in everyone's minds. Like any major deal, it should have been gamed out by M&A internal and external resources taking into account the regulatory environment before it makes the light of day.

- If regulatory hurdles are overcome, what conditions will there be? AT&T has proactively said that the Chicago 700 MHz A Block will be sold. (It doesn't like the A block anyway). Will the company need to divest in other markets (planned or unplanned)?