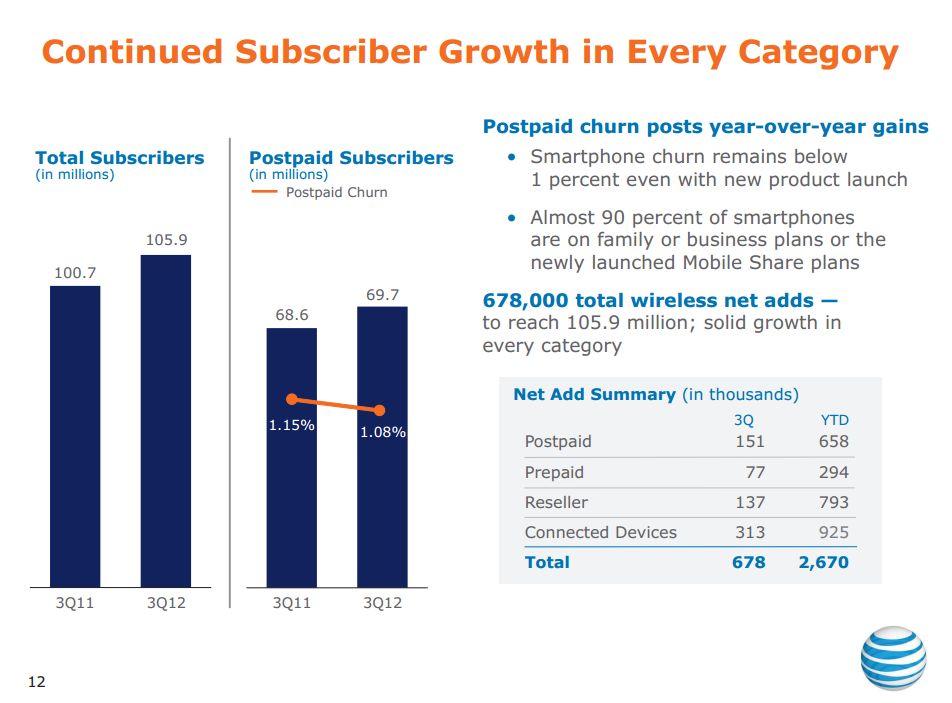

Overall Net additions of 678,000 were disappointing particularly in the postpaid segment with only 151,000. Mobility CEO Ralph de la Vega noted that iPhone 5 supply constraints limited the segment's performance and most of that inventory serviced the existing loyal iPhone base. However, it's hard to not compare to rival Verizon Wireless' Q3 1.535 million postpaid net add number. Nice stats thrown out:

- Smartphones made up 81% of the postpaid sales. Followers should note that Q2 delivered 77% in comparison suggesting that the carrier is doing a good job in pushing the mobile data utility proposition. As a gauge with Verizon, smartphones made up 79% of its postpaid sales. AT&T appears to be doing slightly better job in nailing down data users.

- 6.1 million smartphones activated, 4.7 million were iPhones leaving 1.4 million to be split among Android, Windows and BlackBerry platforms. Interestingly, AT&T did not provide the iPhone 5 breakdown that Verizon presented (650K). We can just assume that AT&T did well since they reported record iPhone 5 preorder/sales during launch weekend.

- About 64% of the postpaid base are smartphone users.

Commenting in the Q&A for the future, Ralph mentioned two things that stuck:

- Q4 postpaid net adds should increase with help from tablets and the mobile share plan. To be fair, mobile share impact wasn't as AT&T expected. Verizon Wireless' data share plan was out of the gate sooner. The thinking is that as new LTE tablets (iPad mini, Asus Vivo and Samsung Smart PC, Kindle Fire) become options (thinking promos here), subscribers would see the value in sharing data.

- AT&T wasn't going to play the traditional net addition game. I assume this was in the context of driving revenue. Rather, revenue was going to be layered service such as Digital Life, a remote monitoring and automation platform that has consumer/business direct services and wholesale partnership opportunities. The company showed a demo of what could be at a house during the spring CTIA 2012 in New Orleans.

On the prepaid side, the trend continued downward for a year. The 77,000 net additions were the lowest since Q1 2011 which was 85,000.

Again in comparison against Verizon Wireless which delivered 228,000 net additions this quarter, this should be a wake-up call to AT&T's prepaid group which represents over 7% of the 105 million base. Given the industry acknowledging that prepaid is a growth segment, AT&T should be playing stronger.

Churn trends were a bit upward. The important postpaid value of 1.08% didn't beat last quarter's sub 1%. Overall churn at 1.34% was higher than Q2's 1.18%; this may be attributed to prepaid and wholesale.

ARPU (postpaid) continued an upward trend at $65.20 but didn't cross $66. That may have been optimistic on my part. Still AT&T continues to lead the industry in this category with a formidable cushion compared to Sprint and Verizon Wireless. Though the mobile share plan didn't have much opportunity to take full traction in Q3, offering an Average Revenue per Account metric was premature. Still, that should be the future path (2013?) if mobile share continues to gain subscriber traction.

EBITDA margin did not match Q2's 45%, coming in at 40.8%. The company's annual guidance of 42.5% was reiterated in slides. Again with Verizon Wireless' 50% figure in comparison, the gap is formidable.

The LTE Network is rolling out ahead of schedule. There is no doubt that meeting the Verizon buildout challenge is key to negate any marketing advantage. Though AT&T's LTE completion timetable is at the end of 2013, Verizon's revised mid-2013 completion provides some incentive to report further accelerations in coming quarters.

Investor Relations

Finally, one must give credit to AT&T Investor Relations for using social media in talking up quarterly earnings. This is the second quarter that I recall that AT&T has done this. Some may dismiss this as another element in public relations but that's the point - put an executive face and provide commentary to frame the quarter's messaging.

Hopefully, more IR websites will incorporate this approach and supplement the dry (but useful) presentation files, archived webcasts and 8K, 10Q/10K links.