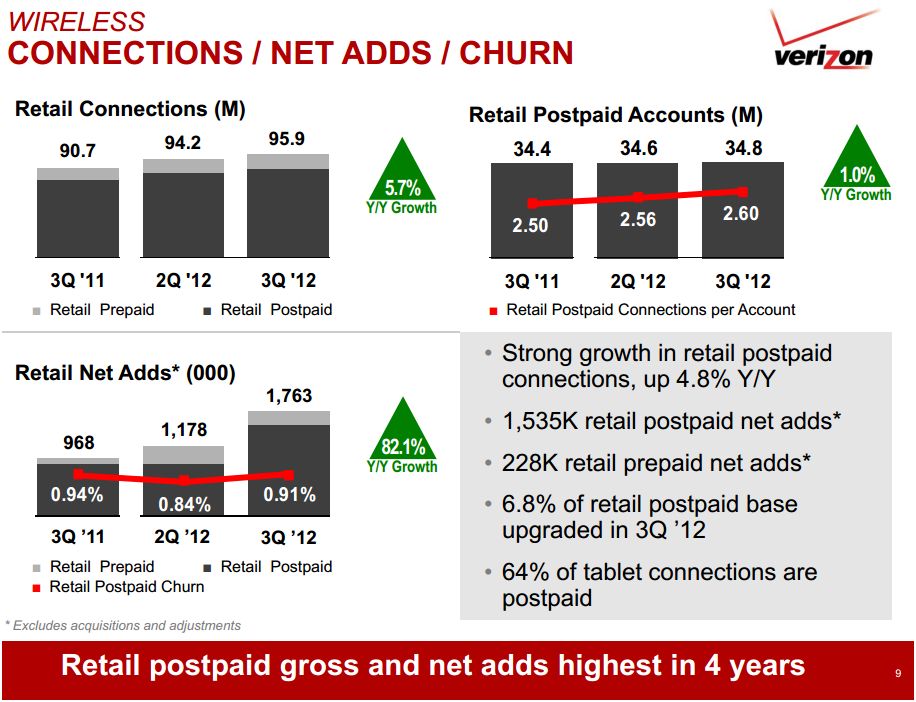

Net additions were impressive - the best performance in 4 years. The metric is always an indicator of organic growth/switching and how the company is performing in postpaid and prepaid. Verizon specifically uses the term retail to pull out any wholesale component.

What stands out is the monster net addition count.

Postpaid: This is the shining beacon for Verizon Wireless with 94% of the retail base in this category. The 1.5+M postpaid is the highest ever. As a gauge, Q2 2011 yielded 1.25+M net adds. Of course part of the strong addition growth comes the shared data plan platform in which tablets (there is even a bullet point on tablets) and data devices (mobile hotspots) are contributing.

Additional notable call highlights supporting the segment's performance:

- Highest gross additions in 4 years at 6.8 million

- Sold: 3.4 M Android smartphones, 3.1 M iPhones (650K iPhone 5s - hampered by supply constraints) - this punctuates the power of Apple. The iPhone sold also show the carrier's switching and upgrade strength - 4/4s iPhones are still desired.

- 78.8% of smartphones sold were postpaid vs. YoY of 59.6% - yes, they're successful partly because of admitted marketing ramp up.

- 53% of the base postpaid base is smartphones and ~9% is internet (devices) so there is room for smartphone growth which suggests average revenue per account has upside potential.

- Switchers: 31% of adds were new to Verizon Wireless. This shows the the network 4G LTE messaging is resonating and helping.

- Smartphone Upsell: 44% of the gross adds were new to smartphones

Prepaid: From a quarterly trend view, this quarter dipped below Q4 2011's 250K and less than last quarter's 299K net adds. Though the segment is positive, we have to watch for its trajectory as the company exits Q4. A consideration may be that the company is putting a great effort in the seemingly more profitable postpaid segment.

Churn: While this looks alarming relative to the previous quarter, this quarter's .091% betters YoY's .094%. Besides, historically, Q2 churn has always been lower so the trend continues. Honestly, this is a boring (albeit great story) every quarter.